statsmodels.stats.stattools.robust_kurtosis¶

-

statsmodels.stats.stattools.robust_kurtosis(y, axis=0, ab=(5.0, 50.0), dg=(2.5, 25.0), excess=True)[source]¶ Calculates the four kurtosis measures in Kim & White

Parameters: y : array-like

axis : int or None, optional

Axis along which the kurtoses are computed. If None, the entire array is used.

ab: iterable, optional

Contains 100*(alpha, beta) in the kr3 measure where alpha is the tail quantile cut-off for measuring the extreme tail and beta is the central quantile cutoff for the standardization of the measure

db: iterable, optional

Contains 100*(delta, gamma) in the kr4 measure where delta is the tail quantile for measuring extreme values and gamma is the central quantile used in the the standardization of the measure

excess : bool, optional

If true (default), computed values are excess of those for a standard normal distribution.

Returns: kr1 : ndarray

The standard kurtosis estimator.

kr2 : ndarray

Kurtosis estimator based on octiles.

kr3 : ndarray

Kurtosis estimators based on exceedence expectations.

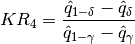

kr4 : ndarray

Kurtosis measure based on the spread between high and low quantiles.

Notes

The robust kurtosis measures are defined

where

is the estimated quantile at

is the estimated quantile at  .

.[R58] Tae-Hwan Kim and Halbert White, “On more robust estimation of skewness and kurtosis,” Finance Research Letters, vol. 1, pp. 56-73, March 2004.